Local European broadcasters are facing ever-increasing competition and severe disruption in a number of areas. Most significantly, they are competing with global digital giants on their home turf within their core business — the TV advertising ecosystem. Furthermore, rapidly changing consumer habits, especially with regards to how and where TV content is consumed, are already having a significant impact on the reach of traditional TV. Various new services with compelling content offerings are driving users away from pre-scheduled linear TV consumption. These topics have become the focus of major strategic decisions, and will unarguably impact the future of the TV broadcast industry.

Broadcasters are not standing idle waiting for the future to be defined for them. In fact, they are investing heavily in technology, content, and new applications that resonate with users and advertisers alike. In recent years, advertising products that are based on the Hybrid Broadcast Broadband TV standard (HbbTV) have rapidly grown in terms of formats and revenues. With HbbTV, broadcasters have started to introduce the addressability of the traditional TV ad break. It appears the industry is at the forefront of a fundamental shift in the traditional TV ad business.

When it comes to offerings on Connected TVs (CTV), broadcasters are showing remarkable success with their Broadcaster Video on Demand (BVOD) offerings. On average, more than 50% of households in the biggest five European markets own a Connected TV, which drives usage on these services. For instance, in Germany, 51% of the total population regularly uses the BVOD offering of German broadcasters. And almost every major European broadcaster provides high-class applications — including addressable advertising products — that offer access to live or on-demand content.

In a bid to increase scale and ease of access for consumers, several major broadcasters have also joined forces to form joint services (e.g. Salto, LOVEStv, Joyn). A rapid increase in ad revenues and subscribers shows that these investments are undoubtedly paying off. European broadcasters are in a strong position to provide future-proof products and services that build the foundation for sustainable long-term business growth.

The market perception of existing Addressable TV (ATV) advertising products is complex and fragmented. This is due in part to the fact that different markets use different terminologies, as do different players within those markets. Specifically, when considering ATV advertising via HbbTV, or within OTT TV services and BVOD applications, there is much confusion. And when it comes to strategic decisioning, all of these are often considered separately. This article seeks to bring clarity, demonstrate why ATV is not tied to a specific platform, device, or form of content consumption, and point to a more holistic approach.

Broadcast, OTT, BVOD – Oh, My!

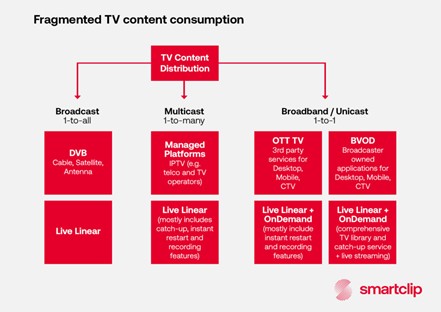

The consumption of TV content is fragmented, and this poses a real challenge for broadcasters. Consumers today expect not only to have round-the-clock access to the live TV stream but also to comprehensive content libraries via state-of-the-art applications on each and every device. Broadcasters are fully aware of these viewer expectations, yet these are also problematic when it comes to providing seamless addressable TV advertising products to advertising clients. Below, we break down the various ways in which TV content is distributed, both via broadcast TV and web-based services.

- Digital Video Broadcasting (DVB): DVB is the conventional live linear broadcast TV through satellite, cable, or antenna. The pan-European HbbTV standard has played an important role in advancing ATV advertising through DVB. The HbbTV standard, which most smart TVs in Europe carry, enables ATV advertising in non-proprietary and broadcaster-controlled TV ecosystems.

- Managed TV Platforms: Managed TV platforms are usually controlled by operators, such as a telecommunications company, who offer an Internet Protocol TV (IPTV) product that usually requires a proprietary Set-Top Box (STB) for receiving the operators’ linear broadcast TV offerings. In operator-controlled environments, STBs act as enabling devices for ATV technology, which must be implemented by broadcasters.

- Over-the-top (OTT) TV: OTT TV services are owned by third parties and provide access to linear broadcast TV bundles via desktop, mobile, or CTV applications. Thanks to the digital nature of OTT, Server-Side Ad Insertion (SSAI) technology makes it possible to exchange and insert spots on the fly within linear live TV streams.

- Broadcaster Video on Demand (BVOD): BVOD applications are broadcaster-owned TV content applications designed for desktop, mobile, and CTV. These include a comprehensive on-demand TV library and catch-up services, and generally offer access to live TV streaming.

Advertisers demand more data-driven products

There is no doubt that advertisers will continue to demand products that enable granular targeting within broadcaster content on each and every platform. Digital competitors are fuelling this demand by offering platforms that provide advertisers with exclusive and advanced data and targeting capabilities. Broadcasters are making a number of strategic moves in the efforts to evolve their content and product strategies to meet this demand.

We are already seeing HbbTV-based ATV advertising products grow at a rapid pace across Europe. Ad formats such as the L-shaped display ad have already proven to create sustainable business opportunities for broadcasters and advertisers. The focus has now moved to enabling the addressability of any placement within the traditional ad break.

Broadcasters are also heavily investing in the provision of linear live and on-demand content on CTV devices through their BVOD applications and on OTT TV services. A large variety of advertising products is already available on the market. Here, substituting ads within the ad break is achieved by applying server-side-based technologies (SSAS).

Pressure is mounting for broadcasters to further develop these digital capabilities, and ATV advertising via HbbTV or BVOD platforms represents one of the biggest opportunities.

ATV advertising represents a major opportunity, whether served via HbbTV or within BVOD environments

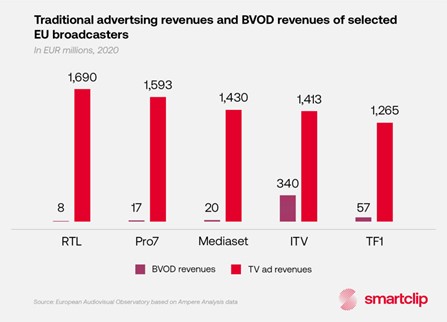

Looking at the advertising revenue of Europe’s largest broadcasters, it is clear that traditional TV advertising is here to stay. Traditional TV advertising is a well-established ecosystem that offers massive scale and proven results. Research shows that advertising within premium TV content significantly improves campaign effectiveness. This is the case for traditional TV advertising, as well as for linear live and on-demand offerings in BVOD applications. Due to the diverse TV landscape, OTT TV services are less prominent and grow on a much smaller scale in Europe.

While the top five European broadcasters generate more than €7 billion through traditional TV advertising, they still do not yet show a significant share of revenue from BVOD advertising. Currently, only ITV is generating significant ad revenue from its BVOD service — the ITV Hub. With over 33 million registered users, it is by far the largest BVOD service in Europe. However, looking at the latest CTV growth numbers in terms of consumption and budgets across all countries, the BVOD advertising market is expected to take off for all major European broadcasters.

In fact, BVOD advertising is showing clear advantages over advertising on other digital platforms. Irrespective of the device, TV and BVOD drive a higher uplift in sales than YouTube, Instagram, and Facebook. This not only points to the importance of traditional TV advertising, but also the need to further invest in new forms of content distribution, such as high-quality BVOD services within web-based platforms (e.g. CTVs).

The status of HbbTV-based ATV advertising shows a similar trend in terms of rapid growth. HbbTV enables the insertion or substitution of ads within the traditional linear broadcast stream. The standard has seen rapid market acceptance and growth. In fact, most leading European TV markets have adopted the HbbTV standard. Germany is setting the pace, with more than 18 million HbbTV-enabled TV devices, and revenue figures in the millions. Meanwhile, Spain has also identified this enormous opportunity — more than 40% of all Spanish households are addressable. Other major markets, including Italy, France, and Poland, also see HbbTV as an opportunity to bring the traditional linear TV business into the digital era.

Lack of market clarity limits strategic decision making and execution

The main challenge is that both HbbTV and BVOD-based ATV solutions are most often discussed separately. There are numerous possible reasons for this. By and large, the technology required to execute these types of advertising products, including proprietary platforms, are provided by different technology vendors who use varying terminology.

Additionally, product and sales responsibilities generally sit in different departments and in turn work in silos. On the buy side, different individuals within agencies are responsible for traditional linear TV buying while others are responsible for digital video buying. This hinders a holistic planning and buying approach, which subsequently leads to limited decision-making and inefficient execution.

smartclip offers holistic solution

At smartclip, we strive to help break down these barriers by providing a one-stop solution for broadcasters and the buy side. Independent of the content stream provided by broadcasters, the smartx platform enables the activation of state-of-the-art, data-driven addressable advertising products. With our smartx platform, we combine traditional linear broadcast with on-demand and live inventories from BVOD services. The underlying standards and solutions, such as HbbTV and SSAS, are seamlessly integrated. As such, inventories from any content stream are collated on the same inventory level within our platform. This allows for a holistic overview when planning and executing campaigns.

For example, our ad server will deliver an ad substitution within an ad break according to supply business rules, targeting criteria, and availability — regardless of the technology through which the content stream is provided.

This also applies to the demand side and buying capabilities. Regardless of IO or programmatic buying tactics, buyers have access to video ad inventory from any of the broadcaster inventory sources. This allows targeted video ads to be bought within premium broadcaster content on traditional TV and/or BVOD on CTVs through the same platform.

The time is now

It is evident that broadcasters have entered into an era in which they are facing significant competition from new global market entrants. Although it may seem as though they cannot defend against these global digital giants, it is clear that they have the assets to create competitive products and future strategies.

The TV advertising business has become one of the most critical battlegrounds. Broadcasters have proven that they are capable of creating products that meet the evolving needs of our market and represent viable alternatives to global digital platforms. The main focus should be on further investment into ATV advertising solutions, regardless of platforms and streams. As such, providing addressable inventories to the demand side in a holistic manner is essential.

Our goal at smartclip is to incorporate all distribution streams and ATV advertising products on one holistic platform. This includes supply-side and buy-side solutions that allow seamless campaign planning and execution across all platforms. Advertisers should have a smooth and unique entry point to execute and optimise ATV campaigns within broadcaster content — and smartclip enables exactly that.

Source: smartclip.tv