The findings detailed in the first instalment of the research company’s COVID-19 Barometer, are based on a survey of more than 25,000 people across 30 markets between the 14th and 23rd March. Due to the time it takes to put together research and the speed of the virus’ spread, at

the point of analysis there were 200,000 cases worldwide (there are now well over 400,000).

Markets are categorised as:

- Early - few cases, limited social distancing policies in place

- Mid – community transmission with social distancing measures in place

- Late – Significant cases and deaths with full lockdown in place

At time of analysis, Italy and China were the only countries examined in the late stage.

What brands need to do:

- Look after your employees and help national/global efforts where possible. Globally, 78% expect companies to worry about their employees’ health, and to favour flexible working, followed by 62% saying staff should be able to work flexibly.

Elsewhere, supporting hospitals (41%) and being helpful to government (35%) is an expectation of significant minority of consumers. - Continue advertising for the long-term. Just 8% of consumers expect brands to cut advertising, so there’s little risk of it being read as insensitive. The risks of going dark by cutting back costs radically can be huge in the long-term, even if there is little short-term effect, according to longstanding Kantar figures.

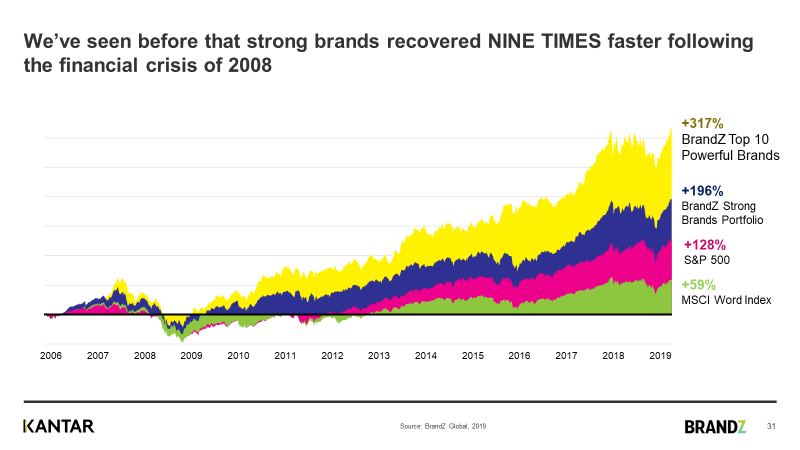

What’s more, it matters for recovery. According to a Kantar/BrandZ analysis of brands following the 2008 economic crisis, strong brands recover nine times faster than the S&P 500 standard.

- What consumers want brands to do during the crisis: help them. Top three comms strategies among consumers include talking about how the brand is helpful in the new everyday (77%), keeping them informed about the brand’s reaction to the new situation (75%), offering a reassuring tone (70%)

- What not to do. It is a tricky line to walk, however, as 75% of respondents agreed brand should not “exploit” the COVID-19 situation to promote the brand. Forty percent of the sample believes brands should avoid humour.

The media picture

Unsurprisingly, media use grows across all countries as they move deeper into the pandemic and more people stay home. Under lockdown, web browsing grows 70%, linear TV viewing increases 63%, and social media 61%.

In terms of gathering information, people across the world exhibit relatively low trust in the sources available to them. Just over half of people worldwide (52%) identify national news media as a “trustworthy” source. But just 48% say the same of government agency websites.

At an app level, Facebook-owned Whatsapp has seen the greatest gains at 40% overall, but usage differs by stage versus typical usage:

- Early: 27% up

- Mid: 41% up

- Late: 51%

In China, social apps WeChat and Weibo saw a 58% increase. Meanwhile, now locked-down Spain saw a 76% increase in Whatsapp use even in the mid stage.

The Kantar figures hint at the sore spot in which Facebook finds itself. Despite its own finding that time spent on all its apps is up 70%, and Kantar putting usage of Whatsapp, Facebook, and Instagram up 40% among under-35s, much of that digital attention is going to be tough to monetise as brands cut digital spend. Meanwhile, those apps’ running costs and extra capacity will weigh heavy on the company.

Source: origin.warc.com